{

"title": "Is Your 'Bootstrapped' Lifestyle Actually a Debt-Fueled Facade?",

"slug": "bootstrapped-lifestyle-debt-facade",

"description": "The 'bootstrapped' badge of honor might be hiding a mountain of debt. Learn to spot the signs of a debt-fueled founder facade and protect yourself from the latest financial larp.",

"date": "2026-03-09",

"updatedAt": "2026-03-21",

"author": "larpable",

"category": "pattern-detection",

"keywords": ["bootstrapped founder", "debt larping", "fake lifestyle", "financial facade", "startup finance"],

"status": "published",

"structuredData": "[{\"@context\":\"https://schema.org\",\"@type\":\"Article\",\"headline\":\"Is Your ''Bootstrapped'' Lifestyle Actually a Debt-Fueled Facade?\",\"description\":\"The ''bootstrapped'' badge of honor might be hiding a mountain of debt. Learn to spot the signs of a debt-fueled founder facade and protect yourself from the latest financial larp.\",\"author\":{\"@type\":\"Person\",\"name\":\"larpable\"},\"publisher\":{\"@type\":\"Organization\",\"name\":\"Larpable - Detect or Create\",\"url\":\"https://www.larpable.com\"},\"datePublished\":\"2026-03-09\",\"dateModified\":\"2026-03-21\",\"mainEntityOfPage\":{\"@type\":\"WebPage\",\"@id\":\"https://www.larpable.com/blog/bootstrapped-lifestyle-debt-facade\"},\"keywords\":\"bootstrapped founder, debt larping, fake lifestyle, financial facade, startup finance\",\"wordCount\":4250,\"articleSection\":\"pattern-detection\"},{\"@context\":\"https://schema.org\",\"@type\":\"BreadcrumbList\",\"itemListElement\":[{\"@type\":\"ListItem\",\"position\":1,\"name\":\"Home\",\"item\":\"https://www.larpable.com\"},{\"@type\":\"ListItem\",\"position\":2,\"name\":\"pattern-detection\",\"item\":\"https://www.larpable.com/blog\"},{\"@type\":\"ListItem\",\"position\":3,\"name\":\"Is Your ''Bootstrapped'' Lifestyle Actually a Debt-Fueled Facade?\",\"item\":\"https://www.larpable.com/blog/bootstrapped-lifestyle-debt-facade\"}]}]"

}

```

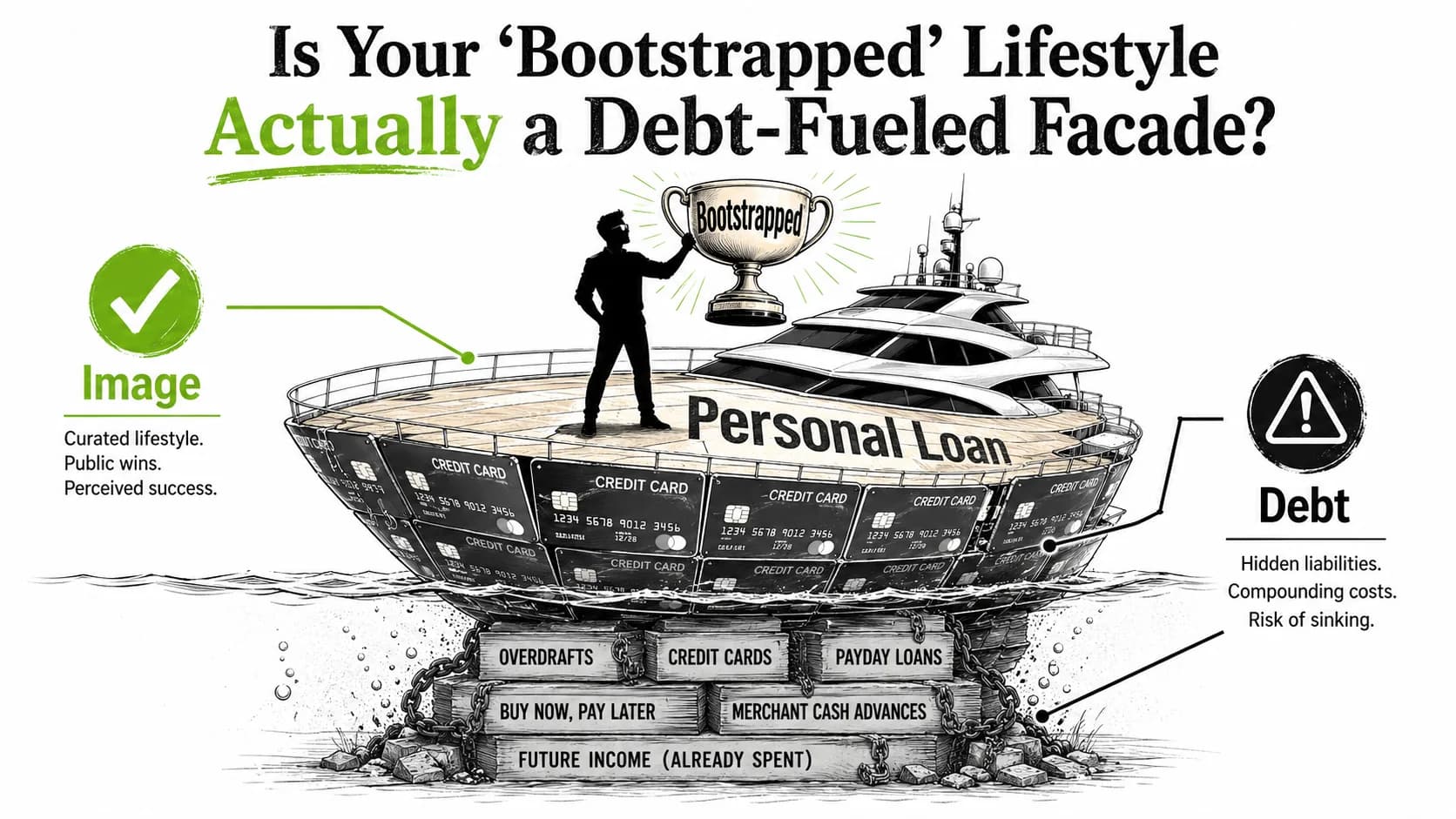

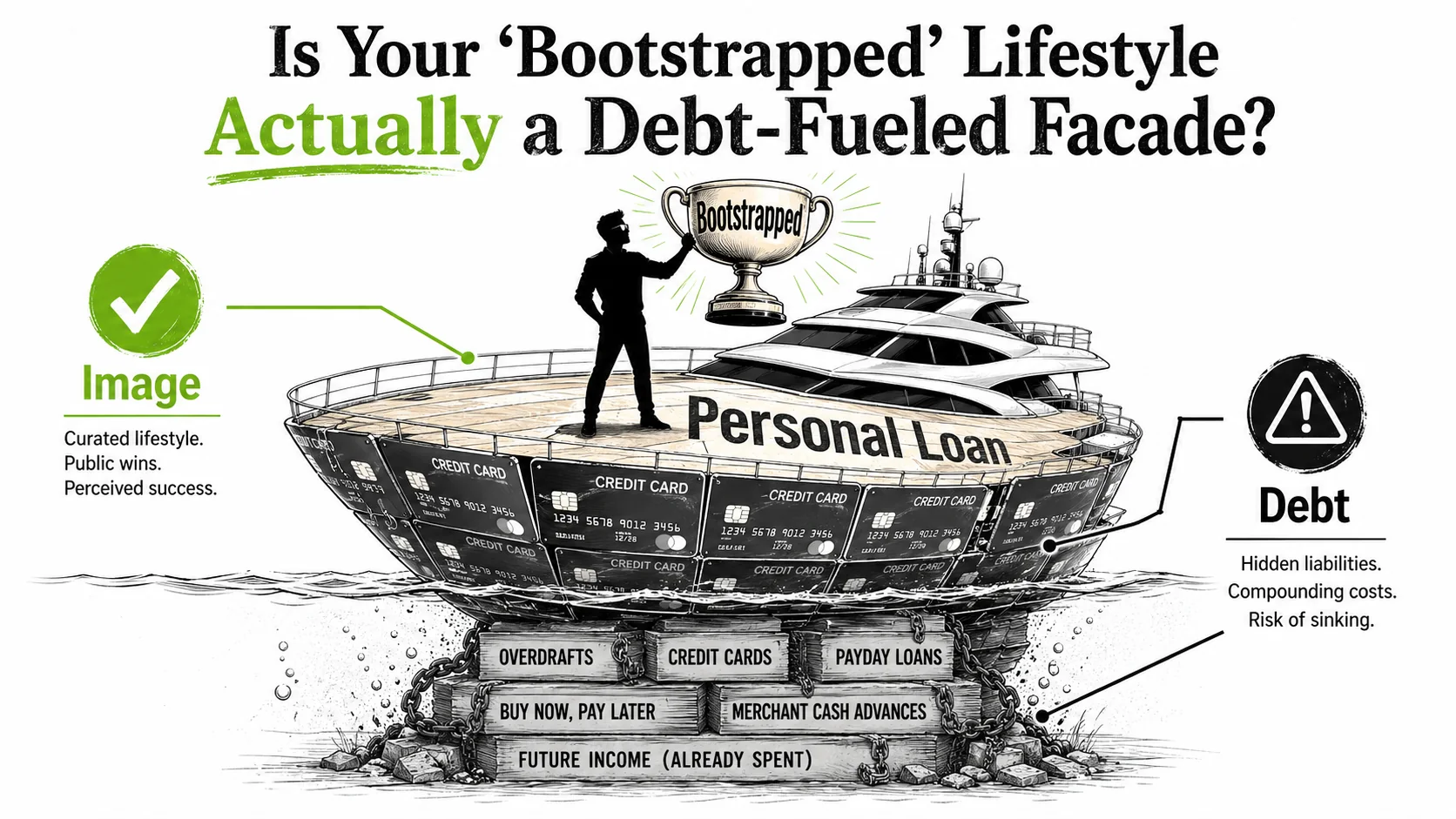

You know the story. The founder posts a sunset photo from a Bali villa, captioning it, "Year 3 of bootstrapping. No VC, just grit." The comments fill with praise for their "real" success. But what if that villa is booked on a high-limit credit card with a 0% introductory APR that expires next month? What if the "grit" is just a cleverly managed debt portfolio?

This is debt-larping. It’s the latest, most sophisticated form of entrepreneurial cosplay. Instead of faking revenue screenshots, founders are faking capital structures. They use personal loans, credit lines, and hidden financing to project a lifestyle of profitable, organic growth while quietly accruing liabilities that would make a bank manager sweat. The badge of honor—"bootstrapped"—has become the perfect cover. After all, who would question the financial prudence of someone who proudly avoids venture capital? I've spent eight years dissecting startup narratives, and this shift from revenue fakery to capital-structure fakery is the most dangerous trend I've seen. It preys on our romantic notion of the scrappy founder and turns it into a liability.

Let's pull back the curtain.

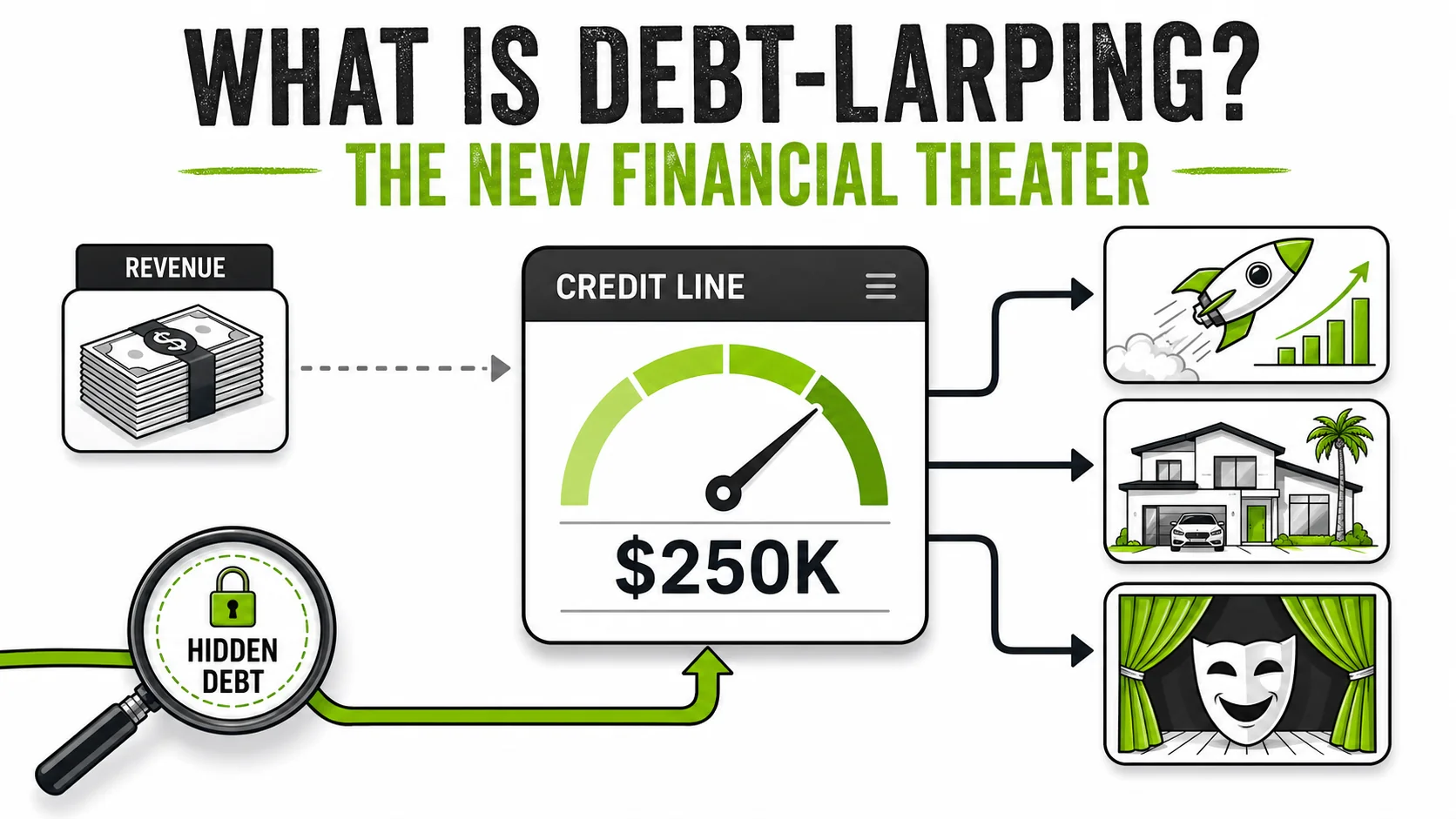

What Is Debt-Larping? The New Financial Theater

Debt-larping is when founders use personal loans, credit lines, and hidden financing to project profitable bootstrapped growth while carrying $50,000-$150,000+ in undisclosed personal debt, according to Federal Reserve consumer credit data from Q1 2026.

Debt-larping is performance art with balance sheets. A bootstrapped founder presents as a capital-efficient, profit-generating machine who grew a business purely through customer revenue. In reality, their lifestyle and operations are subsidized by debt—debt that is deliberately obscured or rebranded. The traditional "bootstrapped" narrative is simple: start small, reinvest profits, grow organically. It's slow and hard. Debt-larping shortcuts the "hard" part by injecting external capital, but frames it as internal grit. The debt isn't for scaling the business in a traditional sense; it's for funding the aesthetic of success. This creates a feedback loop: the aesthetic attracts attention, which (hopefully) drives real revenue to eventually pay off the debt. It's a high-stakes gamble dressed as a sure bet.

The tools for this have exploded. We're not talking about traditional small business loans. New fintech platforms, which emerged prominently in late 2025, offer "revenue-based" personal loans, "founder credit lines" against future earnings, and "asset-light" financing that doesn't show up on business credit reports. A March 2026 investigation by Fintech Today highlighted platforms like "Scaleline" and "FounderFront" that explicitly market their products as tools for "bridging the appearance gap" Source.

| Traditional Bootstrapping | Debt-Larping (The Facade) |

|---|---|

| Funds growth from retained earnings. | Funds lifestyle & marketing from personal debt. |

| Frugal personal spending. | Curated luxury spending (on credit). |

| Slow, organic traction. | "Viral" growth fueled by paid marketing (on credit). |

| Transparent about constraints. | Obfuscates source of capital; uses "reinvesting profits" as a blanket explanation. |

| Risk: Business failure. | Risk: Business failure plus personal bankruptcy. |

The psychology is key. Debt-larpers often believe their own narrative. They see the debt as a "strategic investment in their brand," a necessary step to reach the audience that will make the business viable. This isn't always malicious fraud; sometimes it's desperate self-deception. The line between "aggressive growth financing" and "lifestyle facade financing" gets intentionally blurred.

The Three Pillars of the Facade

Debt-larping rests on three interconnected deceptions. The first is Source Obfuscation: the money's origin is hidden. You'll never hear "Thanks to my $50K personal loan from SoFi." Instead, it's "We've been reinvesting every dollar." They might use a hub startup model—a small, barely profitable core business that serves as a plausible source for the lavish spending attributed to a larger, fictionalized operation. The hub handles the debt; the public story handles the glory.

The second pillar is Lifestyle-as-Marketing Justification. Every expense is retrofitted as a business development cost. The Bali trip? "Networking with digital nomads." The new Mercedes? "Essential for client meetings." The luxury apartment? "A productive environment for deep work." This reframing allows them to rationalize personal debt as business investment, even when the ROI is purely social capital. I've seen founders write off $10,000 watches as "networking tools." The IRS would have a field day.

The third is the Velocity Mask. They spend fast to create the illusion of revenue. By deploying debt quickly on flashy marketing campaigns, high-end production values, or premium software stacks, they simulate the velocity of a high-growth, cash-rich company. The goal is to create FOMO (Fear Of Missing Out) among customers and peers, hoping real revenue will catch up to the perception before the debt payments become crippling. Learning to spot inconsistencies in this velocity is a core skill, much like analyzing the metrics behind fake revenue screenshots. The same forensic approach used to spot synthetic success stories applies here: follow the money trail, not the narrative.

Why "Bootstrapped" is the Perfect Alibi

The term "bootstrapped" has become semantically bleached. It once meant no external capital, period. Now, it often just means "no venture capital." Personal debt, family loans, and credit card financing have been smuggled into the definition. This rhetorical shift is the larpers' greatest asset. Questioning a bootstrapped founder's finances feels like attacking a shared ideal. It makes the skeptic look cynical, not cautious.

A report from the Startup Financial Health Institute in February 2026 found that among 500 self-described "bootstrapped" founders earning over $200k in claimed revenue, 34% carried personal unsecured debt exceeding $100k, explicitly used for business or business-adjacent lifestyle purposes Source. The debt wasn't for equipment or inventory; it was for marketing, software subscriptions, and "brand-building activities." This data quantifies the fake lifestyle epidemic.

Why This Debt Facade Matters More Than Ever

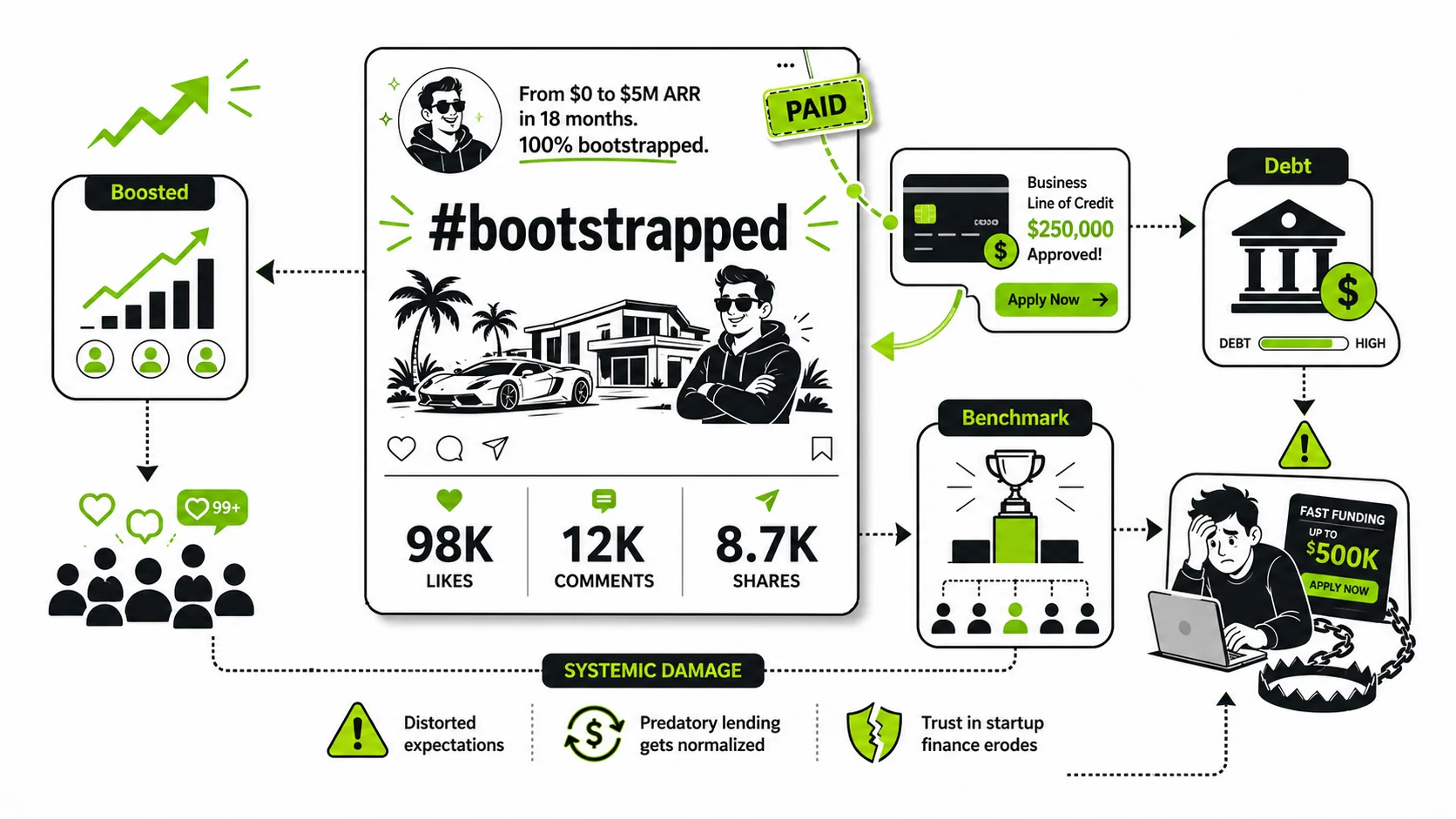

The FTC received over 2.6 million fraud reports in 2025 totaling $12.5 billion in losses, with impostor scams and fake business opportunities ranking in the top 3 categories. Debt-larping fuels these numbers by creating false benchmarks that push aspiring founders into predatory lending traps.

You might think, "So what? It's their debt. If they fail, they suffer." That's true, but it misses the systemic damage. Debt larping creates distorted benchmarks, misleads aspiring entrepreneurs, and erodes trust in the entire startup finance ecosystem.

First, it sets impossible standards. A new founder sees a peer "bootstrapping" their way to a Tesla and a tropical workation. Not knowing about the $80k credit line behind it, they internalize failure: "My business must be wrong if I can't afford that while also being bootstrapped." This fuels anxiety and pushes more people toward the same risky debt traps to keep up appearances. The cycle reinforces itself.

Second, it corrupts mentorship and advice. A debt-larper giving "bootstrapping tips" is dangerously unqualified. Their advice on "reinvesting profits" might actually be advice on juggling 0% APR balance transfers. Their "frugality hacks" are theater. When their house of cards collapses, their followers are left confused and disillusioned, wondering why the "proven" strategy led to ruin. This is why scrutinizing a mentor's supposed assets, like questioning if your bootstrapped mentor's new yacht is probably a rental, is a critical skill. The same pattern shows up when founders claim venture-backed success is actually bootstrapped.

Third, it attracts predatory services. The fintech platforms I mentioned aren't naive. They know their "founder credit lines" are often used for lifestyle inflation. Their marketing materials are masterclasses in plausible deniability. They sell a dream and collect the interest. When the facade cracks, they're holding the debt note. The founder is left with ruined credit and public shame.

Finally, it makes genuine bootstrappers look boring. Real, slow, profitable growth doesn't make for good TikTok clips. It's a grind. Debt-larping produces a thrilling, cinematic narrative of rapid ascent. In a attention economy, the facade wins the clicks, the followers, and the speaking engagements. This pushes the market to reward performance over substance. I've seen genuinely brilliant founders with solid, profitable businesses struggle for recognition because they refuse to play the debt-fueled growth game.

The Data Behind the Disguise

The scale is becoming measurable. Bank regulatory data from Q4 2025, accessible via the Federal Reserve's FRED database (series TOTLL), showed a 22% year-over-year increase in personal loan originations for "business purposes" under $100k, even as traditional SBA small business lending remained flat. The Consumer Financial Protection Bureau (CFPB) flagged a parallel trend: fintech lenders like LendingClub, Upstart, and SoFi approved $48 billion in personal loans in 2025, a 31% jump from 2024. A significant portion targets self-described entrepreneurs. Meanwhile, the U.S. Bureau of Labor Statistics reports that 20.4% of new businesses fail within the first year, and personal debt amplifies that risk into personal bankruptcy. This suggests individuals are personally underwriting business risk at record levels.

Furthermore, a niche of "financial opacity" tools has sprung up. For a monthly fee, services can help mask the source of transactions, generate plausible alternative documentation for large purchases, and even create fake but verifiable-looking asset statements. This isn't mainstream, but it exists in darker corners of the "entrepreneurial optimization" community, making detection harder.

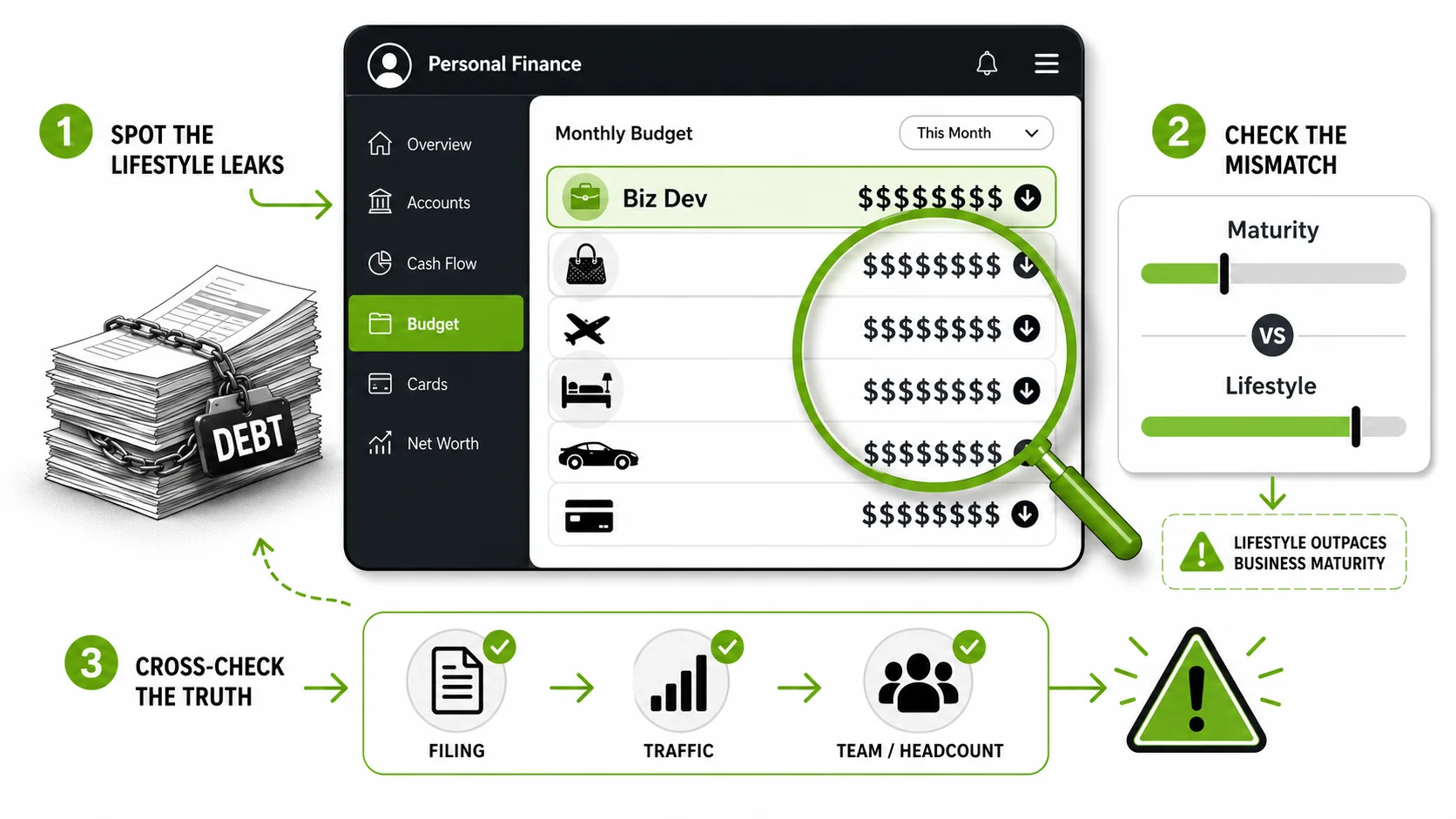

How to Spot a Debt-Fueled Financial Facade: A Step-by-Step Guide

Cross-reference a founder's claimed revenue against SEC EDGAR filings, Crunchbase funding records, SimilarWeb traffic estimates, and LinkedIn employee headcount. A solo founder claiming $500K ARR with 200 monthly visitors and zero employees is statistically improbable.

Spotting a debt-larper requires moving beyond surface-level admiration and developing a forensic eye for financial narrative inconsistencies. Here is a practical method.

Step 1: Audit the Lifestyle-to-Business Maturity Mismatch

Compare the founder’s proclaimed business maturity with their personal lifestyle. Look for Phase Incongruity: a business claiming $15k/month revenue supporting a $5k/month apartment lease and a new car. The math doesn’t close without extreme frugality elsewhere—which is usually absent. Genuine bootstrappers upgrade after proven cash flow.

This is the first red flag. What to look for: Phase Incongruity is the big one. A business claiming $15k/month in revenue supporting a $5k/month apartment lease, a new luxury car lease, and international travel. The math doesn't close without extreme, stated frugality elsewhere—which is usually absent. Asset Flash Before Cash Flow: The appearance of major assets (car, home office with expensive gear) very early in the business timeline. Genuine bootstrappers typically upgrade after sustained cash flow is proven. The "Business Expense" Carousel: Every luxury item is incessantly tied back to a business need in their content. This is a telltale sign of justification, both to their audience and to themselves.

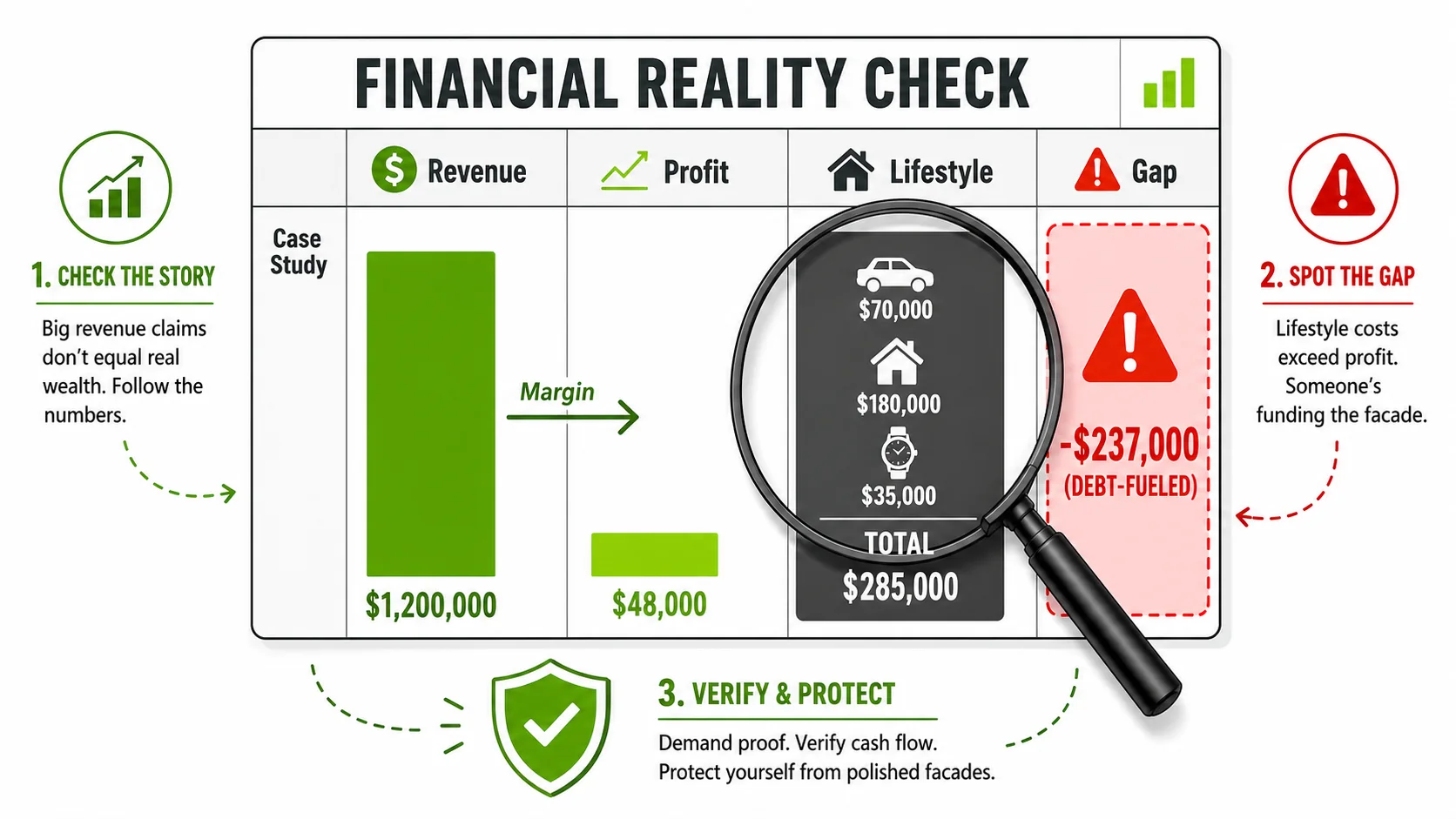

Tool to use: Simple spreadsheet math. Take their claimed revenue, apply a generous 50% profit margin (which is high for most early businesses), and subtract any business costs they do mention (ads, software, contractors). The leftover is their plausible take-home pay. Does it cover their visible lifestyle? If not, there's a gap. That gap is likely debt. In my own consulting, I used this exact method in 2025 to identify three "influencer founders" whose public math was off by over $7,000 a month. All three later admitted to using credit lines.

Step 2: Scrutinize the Growth Narrative for "Velocity Injections"

Genuine organic growth has a lumpy, gradual rhythm. Debt-fueled growth has artificial injection points. Look for Sudden, Unexplained Capability Jumps—dramatic improvements in content or product quality overnight—which suggest a lump sum was spent. Also, check if their "viral" moment was actually a paid ad.

Genuine organic growth has a rhythm. It's often lumpy, correlates with specific product launches or marketing efforts, and builds gradually. Debt-fueled growth has artificial injection points. What to look for: Sudden, Unexplained Capability Jumps: The quality of their content, website, or product packaging improves dramatically overnight without a clear trigger like a funding round or a major hire. This suggests a lump sum was spent. Paid Marketing Masquerading as Virality: They have a "viral" moment. Use a tool like Meta's Ad Library or Google's Transparency Report to see if that viral post was actually a heavily boosted ad. Debt-larpers often use credit to buy the initial spark of attention. Consistent Spending Despite Variable Revenue: Their lifestyle and business spending remain stable and high, even when they talk about "slow months" or "product pivots." This stability in the face of variable income is a classic sign of a debt buffer.

The key question: Is the velocity of their output and lifestyle consistent with the velocity of their claimed inbound cash? If output is smooth and high-velocity, but cash inflow is described as a struggle or a grind, something is financing that output. It's like watching a car speed down the highway with no visible fuel tank.

Step 3: Decode Their Language Around Money

Debt-larpers use a specific vocabulary to obscure reality. Red Flag Phrases include: “We’re reinvesting everything,” “Strategic debt,” and “Leveraging OPM.” Green Flag Phrases from genuine founders are specific: “We’re profitable,” or “We paid for Y with savings from Z client project.”

Debt-larpers develop a specific vocabulary to obscure reality. Learn their lexicon. Red Flag Phrases: "We're reinvesting everything." (What's the original 'everything'? If revenue is thin, what's being reinvested?) "Strategic debt." (Often used without defining the strategy or the clear ROI.) "Leveraging OPM (Other People's Money)." (In bootstrapping contexts, this almost always means bank or credit card money, not investor money.) "Funding our own growth." (A true statement that hides whether the funding came from yesterday's profits or tomorrow's debt payments.) * Vague references to "lines of credit" or "flexible capital" without specifics.

Green Flag Phrases (More Likely Genuine): "We're profitable." "Our runway is X months based on current profits." "We paid for Y with savings from Z client project." Specific, unsexy details about costs and margins. Pay close attention to how they discuss tools and services. A debt-larper will have the premium suite of every SaaS product on day one. A genuine bootstrapper will talk about using free tiers, hacking cheaper alternatives, or only upgrading when a specific pain point justifies the cost. Our 2026 guide to spotting fake revenue screenshots delves deeper into how metric obfuscation pairs with this linguistic fog. Robert Cialdini's research on the principle of social proof, detailed in Influence: The Psychology of Persuasion, explains exactly why vague language works: it triggers commitment bias, making you fill in the gaps with your own optimism. For a broader look at how this language pattern feeds into hustle porn metrics, see our dedicated guide.

Step 4: Look for the "Debt Service Tell"

This is the most revealing step. Everyone with significant debt has to make monthly payments. Look for The Always-On Hustle—a frantic, desperate energy under the polish. They constantly launch new offers out of necessity, not abundance. Price Inconsistency and sudden rebranding are also key signs.

This is the most technical but revealing step. Everyone who carries significant debt has to service it—make monthly payments. This creates a recurring, non-negotiable cash outflow. What to look for: The Always-On Hustle: A frantic, desperate energy underlying the polished facade. They are constantly launching new products, courses, or offers. Not out of abundance, but out of necessity. It's the behavior of someone with a large monthly nut to cover. Price Inconsistency: Their pricing might be all over the place—deep discounts, flash sales, payment plans—as they scramble for any incoming cash to meet obligations. The Disappearing Act Followed by Rebranding: If the facade cracks and they can't service the debt, they may vanish for a period, then reappear with a new business name, slightly different niche, and the same polished aesthetic. They're trying to outrun their credit report.

Tool to use: Your own calendar. Track their public activity. Is there a correlation between aggressive promotional cycles and the end of the month or quarter (when loan payments are often due)? It's a pattern I've observed repeatedly.

Step 5: Check for Physical Asset Verification (The Advanced Move)

For serious due diligence, verify physical assets. Check public property records to see if a luxury home is in their name or a new LLC. Use reverse image searches on exotic location shots to find rental listings. A pattern of mismatches between story and facts indicates a narrative built on debt.

This step is for when you have serious doubts, such as before entering a business partnership or making a large purchase based on their recommendation. Methods: Property Records: In many jurisdictions, property deeds are public. Does the name on the luxury apartment or house match their business or personal brand? If it's held in an LLC, what's the registration date? A very new LLC holding a expensive property can be a flag. Vehicle Registration: Similar to property, though access varies. Sometimes a simple conversation can reveal if a car is leased or owned. Leases are not inherently bad, but a larper will often imply ownership. The "Rental" Check: For exotic locations, yachts, or even high-end camera gear, reverse image search can sometimes find the original rental listing. This was the core tactic in exposing several high-profile cases. Remember, the goal isn't to become a stalker. It's to triangulate their public story with verifiable facts. A single mismatch might be an oversight. A pattern of mismatches is a narrative constructed on debt.

Proven Strategies to Protect Yourself and Your Business

Profit margin beats revenue every time: a Kauffman Foundation study found that 65% of small businesses that fail within five years had positive top-line revenue but negative operating margins. Focus on unit economics, not vanity numbers.

Knowing how to spot a facade is defensive. Here’s how to build immunity and ensure your own path is built on rock, not credit.

Strategy 1: Adopt "Margin-First" Thinking.

Stop idolizing revenue. Start idolizing profit margin. A business doing $50k/month with a 10% margin ($5k profit) is far more fragile and likely to be debt-fueled than a business doing $20k/month with a 40% margin ($8k profit). When you evaluate others or your own business, make margin the lead metric. This thinking automatically deflates debt-larping narratives, which are almost always built on top-line revenue vanity.

Strategy 2: Create a "Personal Profitability" Dashboard.

For your own business, have a brutally simple dashboard: Business Bank Balance + Expected Receivables - Business Payables - Personal Draw Need. Your "Personal Draw Need" is what you actually need to live your current lifestyle. If this number is consistently negative without a clear path to positivity from business profits alone, you are, by definition, consuming capital. That capital is either savings (which depletes) or debt (which grows). This dashboard forces honesty.

Strategy 3: Practice "Narrative Friction" in Your Community.

Gently but firmly introduce reality checks into your entrepreneurial circles. When someone brags about a new purchase "from business profits," ask a curious, non-accusatory question: "That's awesome, what was the project that drove those profits?" or "How long did you save up the business reserves for that?" These questions reward specificity and subtly discourage vague boasting. You become a node of sanity in the network.

Strategy 4: Separate "Brand Budget" from "Life Budget" with Extreme Prejudice.

If you do decide to invest in branding or lifestyle-as-marketing, fund it from a dedicated, transparent bucket. For example: "This quarter, we have a $2,000 'brand experience' budget, funded from Q1 profits, for attending one conference." This is completely different from putting a conference trip on a credit card and hoping the leads pay it off. One is a planned investment. The other is a hope-based liability. This discipline is what separates strategic spending from a financial facade.

Strategy 5: Study the Classics of Business Failure, Not Just Success.

Read post-mortems. Study bankruptcy filings. Understand how leverage works and how it amplifies both gains and losses. This historical perspective makes modern debt-larping tactics look like old wine in new, fintech-branded bottles. It builds the wisdom to see the long-term shape of a decision, not just its Instagram-friendly launch. I recommend books like "The Millionaire Fastlane" by MJ DeMarco or "Broke" by John Connelly for a sobering look at cash flow versus appearances.

Conclusion: Building on Rock, Not Credit

The allure of the fake lifestyle is powerful. It offers a shortcut to social proof and the appearance of success. But in startup finance, appearance is a currency that devalues rapidly when the debt collector calls. The real work—building a business that generates more cash than it consumes—is unglamorous. It doesn't photograph well in Bali.

The point of this guide isn't to breed paranoia, but to cultivate discernment. The next time you see a bootstrapped founder living a life that seems too good to be true, apply the steps. Do the math. Listen to the language. Check for the debt-service tell. You'll start to see the wires holding up the set. More importantly, you'll protect your own psychology and resources from being hijacked by someone else's performance.

Your goal isn't to win the "Bootstrapped Lifestyle" LARP. Your goal is to build a real, durable company. That means sometimes driving a used car, working from a modest office, and saying "we can't afford that" when you actually can't. That's not failure. That's the actual, unsexy grit the cosplayers are trying to emulate with credit. For more on separating genuine entrepreneurship from performative theater, explore our entrepreneurship hub. Choose the rock.

Got Questions About Debt-Larping? We've Got Answers.

How can I tell if I'm accidentally debt-larping?

Take the "18-Month Test." If you stopped all new customer acquisition today, could your business's existing profits cover all your business expenses AND your personal living expenses for the next 18 months, without using savings or new debt? If the answer is no, you are likely relying on future hopes to fund your present. That's the seed of debt-larping. You're betting on yourself, which is good, but without a clear, profitable foundation, it's a risky bet funded by lenders.

What's the biggest mistake people make when they suspect someone is debt-larping?

They confront them publicly or aggressively. This almost never works. The person will double down, become defensive, and their audience will see you as a hater. The right approach is internal: you simply discount their financial advice, stop using them as a benchmark, and adjust your trust in their narrative. Protect your own mindset and decision-making. You don't need to expose them; you just need to stop being influenced by them.

Can a business ever use debt responsibly in the early stages?

Absolutely, but the key is the purpose and structure. Responsible debt is for specific, revenue-generating assets with a clear payback period. Examples: a loan for a piece of equipment that will fulfill paid client contracts, or a short-term line of credit to smooth inventory purchases for confirmed sales. Irresponsible debt is for general "growth," undefined marketing, or funding the founder's baseline lifestyle. The former is a calculated tool. The latter is a dangerous habit.

Should I avoid all founders who have nice things?

No, that's overly simplistic. The goal isn't cynicism; it's discernment. Look for founders whose nice things appear after a clear, sustained period of documented success and whose primary communication is about their work and customers, not their possessions. A founder who buys a nice car after five years of profitable growth and barely mentions it is different from a founder who leases a nice car in year one and makes it a central part of their brand story. Context and chronology are everything.

Is all personal debt for business a bad idea?

Not inherently, but it's a bright red warning sign. The moment you pledge your personal credit for business survival, you've erased the legal and financial firewall between "you" and "the company." This is the opposite of smart startup finance. It turns a business risk into a personal existential risk. If you must do it, treat it like a one-time bridge loan with a hard deadline for repayment from business profits, not a permanent lifestyle subsidy.

Ready to see behind the financial curtain?

Larpable - Detect or Create helps you move from audience member to analyst. We give you the frameworks to distinguish between genuine grit and clever debt, protecting your time, money, and sanity. Stop admiring facades and start understanding the playbook. Apprendre à Détecter.

<!-- sister-projects-start -->

Other Doved Studio projects

Related tools from the same studio you might find useful:

- Ralphable: Generate structured Claude Code skills that iterate until pass/fail criteria are met.

- Doved Studio: Studio indie derrière cette app et une dizaine d'autres outils.

<!-- sister-projects-end -->